“Don’t boil the ocean!” You might have heard this warning-like phrase.

It originates from the literal concept of boiling the ocean, an impossible task. The phrase serves as an advice to not make a task difficult by doing it too thoroughly.

Over time, this advice has become very popular in industry. In consulting, the phrase is something of a blanket–rule that suggests prioritising rather than analysing all the data at hand to arrive at an answer.

Sounds logical, right?

But is this advice equally applicable to ALL?

This advice applies well to large corporations that have such humongous amounts of data, that it is practically impossible to analyse everything. Analysing all the available data to them is akin to “boiling the ocean.” It is time-consuming, costly, and impractical.

So, it totally makes sense for large businesses to “Don’t boil the ocean.”

But, for startups and small & medium businesses (SMBs), it doesn’t make any sense!

For instance, if a small startup is assessing their product market fit (PMF), they must extract every ounce of insight from the little data they have to correctly validate their hypotheses. For them, the data is yet to assume the size of an ‘ocean.’ So, it is perfectly fine for them to try to analyse everything – quantitatively, qualitatively, and contextually – to make the right decisions. Ignoring any data point at initial stages could be the difference between eliminating and selecting their right target customers (or death and growth).

Likewise, for SMBs with small databases, it seems sensible to not follow “Don’t boil the ocean.”

We have experienced this first-hand in our studies for mid-sized clients. Quite often, some nondescript looking data point turns out to be invaluable.

Also, being manically thorough or proverbially speaking boiling the ocean has its own advantages.

Examples galore from every conceivable field, of people becoming exceptionally successful because of being painstakingly thorough.

In fact, it is the only way to be sure of achieving success at anything.

Is it for you?

Then why do many (small) businesses take “Don’t boil the ocean!” as gospel truth?

They do so for three reasons:

1. Propensity to imitate larger successful businesses. When smaller businesses imitate their larger competitors, they are unwittingly doing a favour to their larger competitors. By doing “Don’t boil the ocean,” they are likely to miss on good insights, make wrong decisions, become less competitive, and as a result, miss on becoming a real threat to their competitors.

2. Lack of intent, energy, time, and resources to put in the grunt-work. Let us accept the fact. If you want to be extremely thorough at what you do, you must be prepared to spend disproportionately more time – your time – doing the task. And guess what – it is back-breaking work. Not everybody is willing (or has the energy, time, and resources) to put in the grunt-work. For them, advice like “Don’t boil the ocean” gives a smart-sounding escape. After all, you don’t know what you don’t know.

3. Misplaced priorities. Being thorough correlates with beingeffective. “Don’t boil the ocean” correlates with being efficient. Your first priority as an SMB is to be more effective in addressing your customers’ needs. In today’s information age, deep understanding about your customers and business makes you more effective. If you misplace this priority at the onset, you might end up being efficient in doing the wrong things.

So, Entrepreneurs and Small Business Owners, don’t fall in the trap of management consulting jargon. Reset your thinking!

As the famous saying (in Hindi) goes, “Dikhave pe na jao, apni akal lagaao (rough translation: don’t blindly follow Norself, think for yourself!)”

You are yet to realise your professional and personal goals, So go ahead, and boil the ocean.

If not boil, churn it, get real gems out of it, and enjoy growth!

And large corps: imagine what YOU can achieve if you stop following “Don’t boil the ocean.”

The previous Veracle implored starting a venture not with planning, but tracking.

Tracking has different connotations in different fields. All kinds of tracking have three benefits: predict the future, achieve phenomenal results, and minimise risks.

1. Tracking helps predict the future.

When we track something, we capture a data point.

When we capture data points over time, we observe patterns.

And when we observe patterns over time, we develop predictive capability.

We can use this predictive capability to solve complex problems.

Here is an example from ancient India.

Once upon a time, there lived a mathematician-astronomer – Varāhamihir – in Ujjain. He was a courtier in the emperor’s palace. His correct predictions made him famous as an astrologer.

According to Ancient Indian Hydrology and Brihat-Samhita, Varahamihir used to correctly predict the exact day and prahar (which is a three-hour long subdivision of the day) of the first rains of the season. He could also foretell whether the monsoon would bring enough rains. His forecasts helped the emperor pre-empt and solve water related problems.

Varahamihir had even predicted water on Mars over 1500 years ago. His predictions are still relevant.

But how did they do it in the absence of any advanced instruments?

These scholars leveraged tracking as a tool to develop predictive capabilities.

They closely tracked everything about nature, the celestial objects, and their changing positions. They performed mathematical calculations to draw patterns and conclusions. This helped them connect the dots and understand how it impacted human beings.

In short, when we put tracking to good use, we can solve even big problems.

2. Tracking renders phenomenal results.

Tracking is one of the most underused tools available to everyone.

A little but consistent tracking can lead to remarkable results.

For example, Sachin Tendulkar very diligently tracked every single of the 50,000+ balls he faced in international matches. After a while, he could correctly predict what the next ball is going to be. It helped him bat more balls to boundary irrespective of the opponents or the playing conditions. That made him the legend he is.

On a lighter note, he has tracked the game so well over the years, that he is now being applauded even for his accurate predictions, like this one and this.

John D. Rockefeller, considered the wealthiest American of all time, had developed the habit of tracking the market when he was a regular book-keeper. When the panic of 1857 struck, Rockefeller keenly traced the tumultuous events when the people and businesses around him failed. His tracking habit gave him insights about the weakness in the economy. He used these insights to eventually become the legendary investor.

When we track well, we can achieve the stuff of legends.

3. Tracking minimises risks and avoids unpleasant surprises.

Every field, like business, sports, or personal health, has some ‘performance indicators.’

Close tracking of these performance indicators enables minimizing risks and avoiding unpleasant surprises.

For example, here are some informal indicators to track personal health. Clubbing of fingertips indicates low blood-oxygen, crease in ear lobes may allude to a possible heart trouble, irregular speech patterns, uncommon tongue texture and colour, and abnormal eyes may also reveal presence of some underlying health condition.

When we track our health performance indicators, we can prevent nasty health surprises and ensure longevity of quality life.

In general, when we embrace tracking in our lives, we can predict and control how our life pans out over the years and maximise bliss.

Tracking in business?

Likewise, in business, when we track business performance indicators, we can avoid business catastrophes, predict future performance, and maximise business growth.

We, at Veravizion, have established tracking mechanisms to review business performance. It enables us to identify red flags for our clients early-on and help them grow.

A business tracked well is a business worth running.

What tracking mechanisms do you use to manage your business?

If you check out project success rates, you will be in for a rude shock. A significant percentage of project ventures fail. By conservative estimates, 39% of all projects fail at some point. KPMG puts the estimate at 70%. It’s like, every 2 out of 3 projects fail.

Often, the roots of failure lie in the project planning, or the lack thereof.

Why is the failure rate so high despite availability of so many tools, talents, and trainings?

Clearly, something is wrong.

Most projects follow some variant of the renowned PDCA – Plan -> Do -> Check -> Act – cycle for project planning.

And here is the problem: They start with planning.

But, planning is not the first step of good planning. Tracking is that first step.

Let me explain.

A project objective entails us going from our current position to a desired new position.

For example, a weight loss project involves someone going from 110Kgs to 70Kgs; or your business growth project requires you going from $5Mn to $50Mn.

Planning helps devise the path to go from the current position to the desired new position. Now, the path will take you to the desired position only if the planning is correct.

And the planning will be correct only if it is based on facts, and not on assumptions.

This is where tracking comes in.

Tracking is collecting facts by measuring everything about the current position. Tracking helps us build a comprehensive understanding of all past actions and behaviours (in a person, project, or business) that led it to its current position. This deep understanding helps us plan the right actions which we can practically take to reach the desired position.

Planning without tracking leads to incorrect planning, leading to suboptimal results and project failure.

So, for someone wanting to go from 110kgs to 70kgs, tracking the person’s behaviour helps understand their current position of 110kgs – the person’s body type, eating habits, working schedules, sleeping patterns, propensity to exercise (or not), belief in discipline, and in general the lifestyle.

[Since gym-instructors rarely track all this BEFORE starting the gym routines, it seldom* works.]

Likewise, for a business aiming to grow revenues from $5Mn to $50Mn, tracking the business helps understand its current position of $5Mn – who the customers are, what they buy, why they buy, when they buy, their buying habits, and pretty much everything about the business.

That’s why, tracking must be the first step of any project venture, before any planning.

The initial tracking provides factual inputs to devise the proper plan – the right path – to reach the desired position.

Once a venture starts tracking everything required to prepare the plan, the plan will be real, and executable. It will solve both the planning and execution problems.

Here is one case study.

One of my friends had migraine for many years. It was extremely severe – high frequency, high intensity kinds. In his words, “it would be as if someone is pounding Thor’s Mjölnir continuously on one side of my head, for hours, without break.”

He tried a lot of things, without any substantial results.

I suggested him the above approach. He effort- and time-tracked his entire days – EVERYTHING – for many weeks. Afterwards, we analysed the data. We gathered significant insights to plan the right actions to get rid of his migraine. He is now a relieved person.

In sum, if you want to succeed in your venture, don’t start with planning. Start with tracking instead.

*More than 80% people who have gym membership do not use the gym because it doesn’t seem to benefit them. Only about 18% of members actually went to the gym consistently.

There appears an increasing level of interest among math scientists to work on topics, like machine learning, that are changing people’s lives through its application in business.

“A topic that is attracting more and more attention is mathematical aspects of machine learning. There are many directions; one that interests me is how I could use some of these exciting new tools in my own research. Another very ambitious and noble goal is to create a mathematical theory of machine learning. When does it fail, and when we can we hope for good results?”

— Maryna Viazovska, 2022 Fields Medal winner, in a Q&A with Nature

This Veracle is about how the mathematicians’ work is instrumental in pushing the boundaries of making data-driven decisions in business.

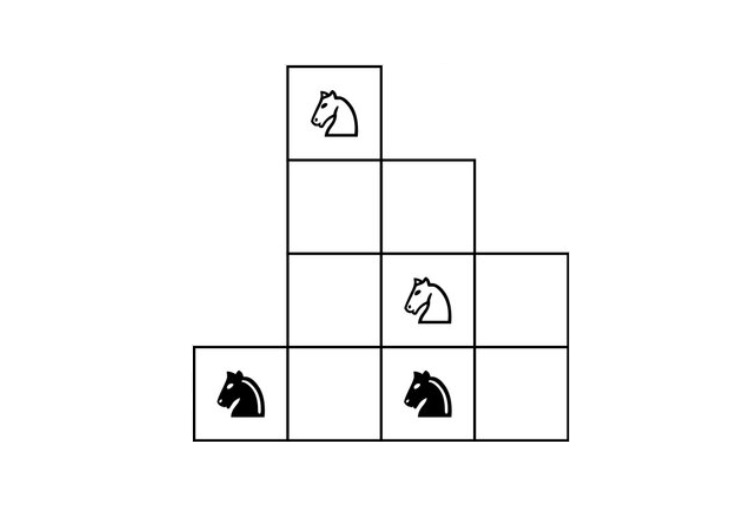

Let us begin with a little fun challenge: Take a look at the four knights on the cover picture. Can you exchange the positions of the black and white knights on the given chess board?

If you can, then you may have it in you to win the Fields medal.

What is Fields Medal and how is it relevant to business?

The Fields Medal is the most* prestigious award a mathematician can receive. The International Mathematical Union presents the medal to young math scientists for outstanding contributions in mathematics. The Fields Medal is only awarded every four years.

The obverse and reverse of the Fields Medal

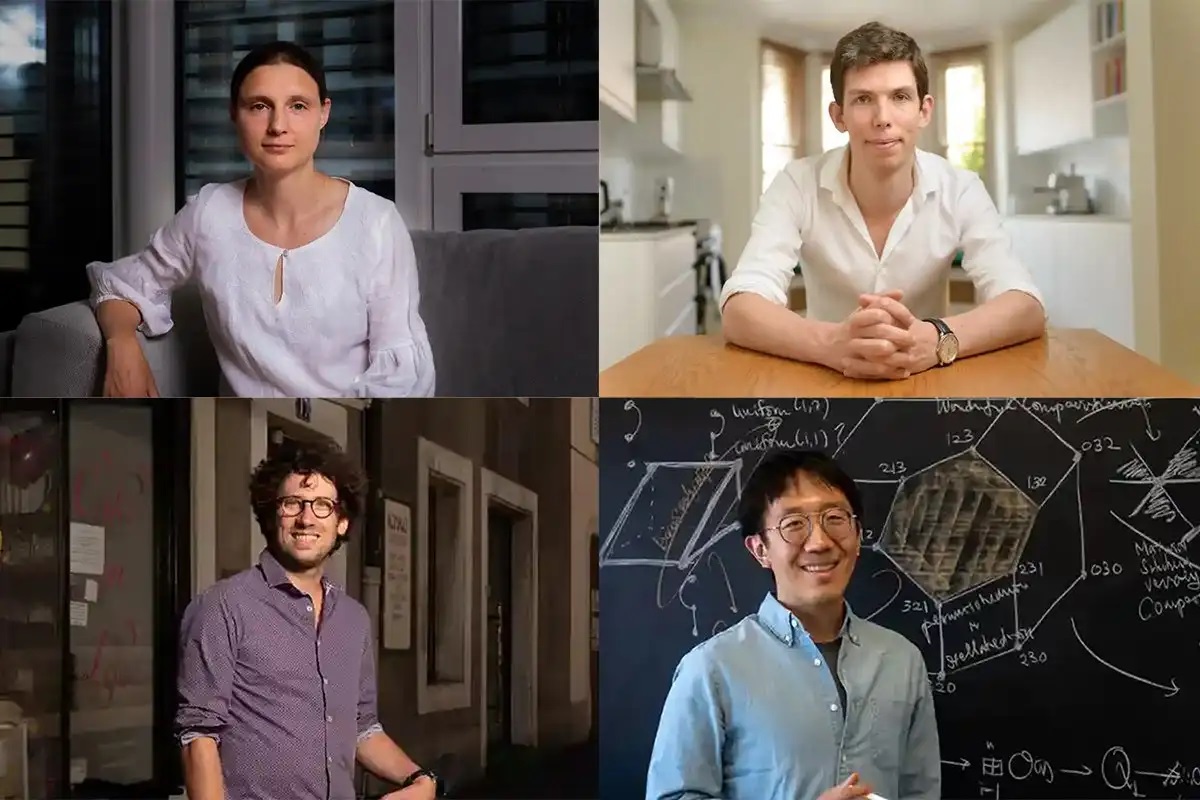

This year, four mathematicians are the winners of the Fields Medal. They received their awards earlier this month in Helsinki, Finland.

2022 Fields Medal winners

They have earned this distinguished honour for solving or moving closer to solving longstanding “open problems.”

An open problem is a known stated problem which has not yet been solved. It is assumed to have an objective and verifiable solution.

The answers to open problems pave ways for innovative ideas and possibilities. In business context, these answers facilitate, among other things, making business decisions better and faster.

How is their work exciting and significant?

Business decision making has become too complex. Business executives must consider both qualitative and quantitative information to make decisions.

Qualitative information uses subjective judgements. This includes non-quantifiable data such as employee expertise, people attitude towards change, and company culture among other intangible aspects.

However, quantitative information uses data. Now, organisations have too much data available to them. They have data generated by operational transactions, market research, and external sources. Organisations must analyse this exponentially growing data to make decisions. Moreover, they must make many of these decisions in the runtime.

To that end, businesses need more advanced computational algorithms to sift through zettabytes of data to analyse and arrive at useful insights. The conventional techniques are highly time and cost intensive.

This is where work of the Fields Medallists becomes significant.

How does mathematics help business decisions?

This year’s Field Medallists’ works are centred on number theory, probabilistic theory, and combinatorics, among other more intricate topics.

Here are a few examples of business applications of the topics of their work.

Number theory deals with the properties and relationships of numbers.

It has helped in public key cryptography, such as RSA algorithm. This has enabled confidential communications, digital signatures, and secure online transactions for e-commerce companies.

Probability theory is the branch of math concerned with calculating the likelihood of an event. It has numerous applications in business.

From all kinds of risk assessment and modelling (like that for investment and insurance) to sales forecasting, most prediction algorithms use probability theory.

Combinatorics is the study of objects and connections between them. Simply speaking, it has applications wherever we need to arrange things using permutations and combinations.

One can see examples of combinatorics everywhere. It can help in optimising communication networks and logistics. Combinatorics had a crucial role in manufacturing. For example, modular toy manufacturing.

At Veravizion, we help our clients thoroughly understand their customers. The objective is to devise and implement effective marketing strategies for their business growth.

This involves figuring out our customers’ real target customers, understanding their purchase motivations, performing causal analysis, optimising resource allocations, and in general solving their business problems.

In this process, we apply several techniques such as clustering, regression, optimisation, resource planning, and various other statistical analyses. These are based on pure math and statistical concepts like probability theory, combinatorics, and mathematical optimisation.

Are there any areas of business where you think we can consider using math and statistics?

How else does math help businesses?

* The Abel Prize is also regarded as a top award in mathematics. According to the annual Academic Excellence Survey by ARWU, the Fields Medal is consistently regarded as the top award in the field of mathematics worldwide, and in another survey conducted by IREG in 2013–14, the Fields Medal came closely after the Abel Prize as the second most prestigious international award in mathematics.

Analytics is the process of discovering, interpreting, and communicating meaningful patterns in data. It helps us make decisions based on data and hard facts.

Most companies now use analytics to make data-driven decisions. They expect that good insights can really take their business to the next level.

Unfortunately, good insights rarely emerge.

Is analytics all hype then?

Here is a startling finding.

Research by PwC and Iron Mountain indicates that three in four businesses extract little or no advantage whatsoever from using analytics. According to the study, 43 percent of companies surveyed “obtain little tangible benefit from their information,” while 23 percent “derive no benefit whatsoever.”

Now, everyone and their uncle is claiming to use analytics in their business. If it was really useful, the world’s GDP have gone through the roof.

So, why are businesses not able to leverage analytics?

This HBR article and the PwC research discuss the root cause. Both studies point to lack of the right capabilities and competencies required to make good use of the information companies have.

This finding really warrants the question. What capabilities and competencies do we need to extract real value from data?

In fewer words, what makes analytics valuable and beneficial?

The answer is STATISTICS.

Statistics makes analytics insightful.

Analytics without statistics is bland, blunt, and bootless. It is like Ron’s broken wand in (the Harry Potter movie) The Chamber of Secrets.

Analytics without statistics, at best, gives us dull observations like ‘focus on the millennials.’ At worst, we get costly and impractical recommendations like ‘redesign the entire supply chain.’

This lack of benefits from analytics leaves businesspeople disappointed.

An analysis is ‘insightful’ when it goes beyond the superficial. It gives an accurate and deep (hitherto unexplored) understanding about the subject. Besides, an insightful analysis helps us break our long-held beliefs and preconceived notions that hold us back.

Here are two diverse examples of insightful findings.

Example 1: who revolves around whom?

The western world during Aristotle’s time (c. 384 B.C. to 322 B.C.) believed that the Sun revolved around the Earth. For 1,000 years, Aristotle’s view of a stationary Earth at the centre of a revolving universe dominated the studies of the universe. Surya Siddhanta and later Copernicus’ work showed that it was the other way round. That ours is a heliocentric solar system in which the Earth and the other planets revolve around the Sun.

That is insightful.

Example 2: how do you shave?

Gillette first entered the Indian market in 1984. But they failed to sell razors despite trying for many years. They even launched their newest triple-blade system in 2004. However, sales were flat for a long time. Why? Gillette did not understand the Indian consumers. They had tested the product with only a few Indian Students at MIT and hence had missed crucial insights about shaving habits in India. A large part of Indian men did not have access to running water and had longer and thicker hair (than Americans). Based on these enlightening insights, they launched Gillette Guard for the Indian market, tasted success for the first time, and never looked back.

Connecting the dots…

So, how does statistics make analytics insightful?

It does so by employing systematic numerical methods to analyse enormous quantities of data representative of the entire population. Statistics helps us make inferences on the whole population from those in a representative sample. The representative sampling assures that inferences and conclusions can extend from the sample to the overall population.

Ideally, everyone using analytics must incorporate statistical techniques.

But there is one hitch.

In fact, there are three:

Statistics is complex. If there is one subject which is universally hated, it is statistics. Advanced statistics can get overly complicated. If they must, people use only the descriptive statistics which is easier. They tend to stay away from inferential statistics which is responsible for drawing inferences and conclusions.

Use of statistics needs expertise. One needs in-depth understanding of statistics to be able to apply it completely and correctly. Moreover, there are different statistical techniques for different data types. One must identify the right techniques to use depending upon the nature and quantity of data available. Many a times, we need to apply statistics in multiple stages (like the Bonferroni correction) to get more accurate results.

Building expertise takes time and efforts. Naturally, it is costly. It involves having the right people with deep level of knowledge and experience to apply analytics. Most people stop at the basics.

Due to this, it is rare to see use of statistics in analytics. Hence, despite being beneficial for business, useful analytical insights are hard to achieve.

Thus, analytics without statistics is anything but useful. But analytics with statistics is powerful. It delivers meaningful benefits.

That is why, at Veravizion, statistics is the indispensable part of all our analytics and consulting work.

There are several instances where the right kind of analytics (that include statistics) have rendered spectacular results. Analytics is reshaping industries like retail, consumer goods, healthcare, banking, and agriculture, among others. But that is a topic for another Veracle.

What has been your experience of implementing analytics?

We make decisions all the time. Some decisions are easy while others are difficult.

Why are some decisions difficult to make?

It is because they involve a trade-off.

A trade-off is an exchange of something of value for another, usually as a compromise. Simply put, it is a situation that presents us with two or more desirable choices, but we can choose only one.

Easy decisions – involve little or no trade-offs

Difficult decisions – involve tough trade-offs

Naturally, there is a tension involved where you have to trade-off (or lose) something of value for another.

Consider these examples involving trade-offs.

In healthcare, a patient suffering from seizures is offered the choice of brain surgery or long-term medication. The brain surgery can cure the condition but has low probability of success and may impair some other function like speech or memory. Whereas the medication may or may not be highly effective and cause unintended side effects like excessive drowsiness.

It is a gut-wrenching trade-off.

In career, we want a high-paying job having future growth prospects. But it may require frequent travel to different time zones and odd working hours. The decision involves a trade-off between career and health. Moreover, the job comes with the pain of staying away from family.

Unfortunately, such situations are common in business.

In business, a CEO may need to choose between closing the loss-making plant (and firing hundreds of employees) and attempting a turnaround possibly incurring further losses (and risking the survival of the entire business).

Thus, a trade-off implies an opportunity cost, or a sacrifice, or a pain to gain something. And these things hurt. That is why, decisions involving a trade-off are painful and difficult.

A tough trade-off makes us freeze or flee in the face of tough decisions.

How do we resolve a trade-off?

There is an interesting aspect about how the human psychology works when forced to face a trade-off.

In deciding between two options, we like to choose the higher value option over a lower value alternative.

Likewise, we prefer picking the less risky option over the riskier one. This is because human brain equates uncertainty with danger and causes anxiety. So, it wants us to make such decisions quickly to minimize the anxiety and stress.

In short, both the rational brain (i.e., prefrontal cortex) and the emotional brain (i.e., limbic system) are in action.

In such a situation, the key is to listen to the rational brain.

When forced to face a trade-off, be fiercely rational.

This is easier said that done. Because it is extremely difficult to suppress the limbic brain. Only a well-defined process can help.

That is why, to make difficult decisions, we need a rational decision-making process that:

gives us the best value option (with higher probability of success),

is quick and efficient (saving the anxiety and pain), and

helps us achieve the organisation’s purpose and vision.

In business context, the need for such a methodical decision-making process is vital. The analytics based decision-making process fills this space.

Analytics based decision-making process

This process satisfies all the above criteria:

It gives us the best value option. Analytics uses tools like classification and decision trees. These tools evaluate a quantitative value for each decision option. We can compare these values to better assess the trade-offs. We can weigh cost and benefits of each decision. Overall, this process helps us choose the best value option.

It is quick and efficient (and saves from anxiety). Analytics employs proven techniques and frameworks applied on data. These techniques are time-tested and use data as factual inputs. This brings objectivity in the decision-making process. As a result, the process takes away the emotional anxiety and appears unbiased.

It helps achieve our long-term vision. Most importantly, analytics makes use of statistical algorithms based on probability. This entails assessing each decision with the likelihood of achieving organisational objectives.

Thus, analytics based decision-making process helps in achieving organisational objectives in a facts-based, timely, and efficient manner.

More benefits…

There is an additional yet understated benefit in using analytics for decision making.

The approach helps in communicating and justifying the decision to all the stakeholders. The pyramid principle made popular by Barbara Minto uses analytical reasoning to communicate a decision. It enables managers to get buy-in from the shareholders and employees for successful implementation of decisions.

In sum, analytics helps make, communicate, and justify difficult decisions.

What approach do you take to make important decisions?

How do you define your business? Can you tell what business are you really in?

Seriously, do take a moment and complete the following sentence.

I am in the business of ___________________________________.

Why is it important to know what business we are in?

Because it helps us decide exactly what to sell, whom to sell to, and how to sell. Without this clarity, businesses struggle to continue to survive.

Most of us define it based on:

What we do: we print books and brochures; we are in the printing business.

What we own: we own factories and workshops; we are in the manufacturing business.

What products we sell: we sell toys; we are in the toys business.

However, this seller-centric approach is not optimal. What if customers stop using what we do, or stop making stuff with what we own, or stop buying products we sell. We will soon be history.

Then how should we think about what business we are in?

Let us understand with an example.

What business is Amazon.com in?

Amazon.com does packaging and delivery of stuff. Of course, they are a logistics and supply chain company. But they do not earn revenues from trucking and shipping.

Amazon.com owns large fulfilment centres and warehouses to store stuff. Clearly, they are a storage and warehouse company. But they do not profit from rentals and leases.

Amazon.com sells around twelve million products. Sure, that makes them a retail company. Except, they do not make money off the products they sell.

Rather, they make money by earning commissions through sellers. That means they are in asset-light brokerage business, right? But then, they own tons of assets, both physical and digital?!

So, what business is Amazon.com really in?

Amazon.com defines themselves as a customer-centric technology company. They use technology to connect retail buyers and sellers on a unified platform. They use data analytics to understand more about their customers – both buyers and sellers. Amazon leverages these insights so that sellers get more buyers, and buyers get a wider range of selection for cheaper from multiple sellers.

How could Amazon.com have clarity about what business they are in when they do so many things?

Because they do not define their business by what they do, or what they own, or what products they sell.

Amazon defines their business based on what purpose they serve for their customers.

That is the key.

We must define our business by what purpose we serve for our customers.

It keeps us aligned with the customer needs all the time. Moreover, it allows us to pivot with changing customer needs and preferences. Most importantly, it helps us build sustainable competitive advantage and ensures business continuity.

A product does not define a business, the purpose it serves for its customers does.

If products defined businesses, then Sony Walkman cassette player, Ambassador car, Toys “R” Us, Apple Newton, Pontiac, Polaroid camera, Nintendo, Palm Pilot, and many such products would still be around.

Yet, several companies have failed for not developing this clarity.

Kodak helped people create lifetime memories. However, Kodak thought they were just selling photographic films. So, when an engineer (ironically from Kodak) invented a filmless digital camera to achieve the same purpose in a better way, Kodak ignored. Not thinking about what business they were really in, they focused on their product – films. They completely missed the purpose they served.

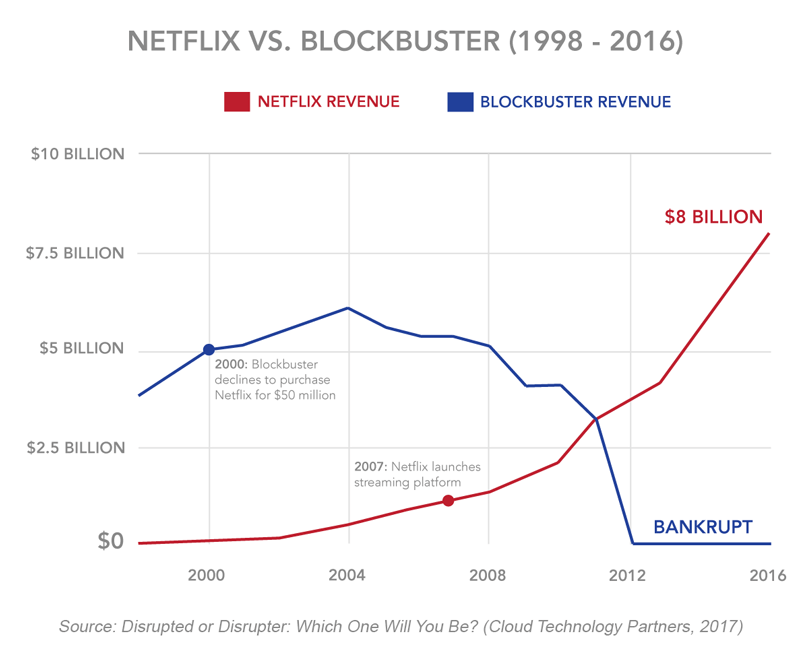

Blockbuster enabled people to enjoy movies at home. But they thought that they were in the business of video rentals. At the time, Netflix also rented out videos by mail. Yet, Netflix figured out that they were really in the entertainment business. This clarity helped them pivot from the mail-based video rentals to DVD rentals to subscription video on-demand (SVoD).

The clarity is essential

To reiterate, we must define our business by what purpose we serve for whom.

Once we build this clarity, it is easier to articulate it to our customers thereby attracting the right customers and propelling our sales forward.

If you are yet to start your business, then why not do so by answering this question: what purpose of which customer do you want to serve?

This article on startup pitch in the Shark Tank India by the author first appeared in the 6th March 2022 edition of the English daily ‘The Hitavada’, in the business insights section of the Newscape supplement.

If you are an entrepreneur, how do you present your pitch to the investors to actually get funded?

Easy-peasy.

Wear your cool company t-shirt, open your presentation with a little stunt involving your product, and use a lot of MBA jargon (in short-forms) to impress the investors.

Right?

Well, not sure if ‘The Sharks’ agree.

Shark Tank India

The show “Shark Tank India” took the nation by storm and managed to catch everyone’s attention. The show brought forth some incredible innovations, fantastic business ideas, and passionate entrepreneurs on screen, leaving audiences inspired and spellbound. The timing of the show couldn’t have been more perfect. Amidst India’s booming startup culture, the show offered an ideal platform for top pitches to make an appearance.

This is especially significant since it is very difficult to get an opportunity to actually present your pitch in-person to serious investors. Yet, it was bizarre to watch so many of them not make the most of this golden opportunity.

Specifically, one could observe two points in the startup pitch:

Firstly, many startups, despite having a terrific idea and a go-getter attitude, had to return empty-handed.

Secondly, while it was exciting to note that more than half of the startups secured some funding, a little analysis of such ventures revealed that many did so at markedly reduced valuations. Consider these insights:

the original valuations by the Founders were brought down in a staggering 95% of the startups.

the valuations of the startups that were funded, were lowered by an average 63%.

only three ventures could justify their valuations. But then, two of them were valued at just Rs. 5.00 and Rs. 101.00 (not missing any zeroes there). Ha!

If you are tempted to blame the sharks then please consider this. The sharks are doing their job alright. (They are called sharks for a reason – they are small, aggressive, and move quickly.)

So, why couldn’t the startups do better in the Shark Tank?

Apparently, the startups are not following a few basic principles of presenting investment proposals.

Here I suggest three actions to prepare a better pitch:

Build deep clarity about your venture.

Develop understanding about investor expectations.

Be comfortable with numbers.

Let me elaborate.

1. Build deep clarity about the business venture.

This sounds elementary yet it is most important. Founders must develop complete clarity on four aspects of their business: the market (or customers), the product (or service), the execution, and the team’s capabilities.

This clarity helps answer questions like:

What gap is the business trying to fill and for which customers?

What does the business offer on a pain-pleasure continuum? The business must either solve a painful problem faced by real people or offer a unique pleasure experience.

Does the business have capabilities to solve it exceptionally well?

How does your business make money?

When you have clarity of thought on the above, you are able to answer all the questions during startup pitch – whether asked directly or disguised in business jargon like B2B/B2C, burn rate, CAC, churn, gross margin model, MVP (Minimum Viable Product), PMF (Product Market Fit), revenue model, runway, traction, valuation, value prop, working capital model, and so many others.

Let me explain one here.

Take Product-Market Fit.

Many startups struggle with achieving the product-market fit because of lack of clarity about target customers and right product positioning. PMF is the evidence that your product perfectly addresses a genuine gap felt by many customers. Be it a consumable or a technology product, the question it answers is: is your product relevant to its customer base?

For example, a popular international doughnut brand could not sell doughnut as a breakfast item in India. Why? Because doughnuts were relished only on special occasions but not as a breakfast option. We Indians are too loyal to our pohas, parathas, and palappam.

Here is the key insight:

If YOU don’t have complete clarity about YOUR own venture, you will never be able to communicate it clearly to those who matter.

2. Develop understanding about investor expectations

Most investors look for evidence of ROI in your business venture through these three questions:

Is it profitable?

Will you be able to scale it or pivot it, as required?

What returns will they get and by when?

Accordingly, the sharks were asking questions intending to seek answers to the above questions.

Hence, it is important to develop this understanding before the startup pitch. It will help you focus your time and efforts on the right sharks that can offer not just money but also their expertise.

The last point is especially important. Many investors are impassionate to the venture; they are there primarily for the financial returns within their expected investment horizon (because they may be investing other people’s money too).

Therefore, be extremely genuine, upfront, and realistic with the investors. Acknowledge that they may understand ‘doing business’ better than you do.

3. Be comfortable with numbers.

When you share information about your venture, why should the sharks believe you? More precisely, what will make them believe you?

The answer is ‘Show and Tell’.

Always supplement your statement with numbers and reliable data. To do that, you must be comfortable using numbers in your communication.

For example,

rather than saying, ‘we are showing phenomenal growth and high profits’,

Say, ‘we are growing 250% Qtr-on-Qtr’ or

Say ‘we sold 42K pieces for Rs. 72Lakhs in 3 months with a gross margin of 68%’.

On the show, the sharks appeared more receptive and responsive to the entrepreneurs explaining their venture with credible numbers.

When you do so, the investors will make the right deductions, and BELIEVE IN YOU.

As they say, nothing speaks like results.

Taking these actions will not only improve the odds to secure funding, but also help entrepreneurs to justify their valuations. You don’t need only banana chips* to do that.

Easier said than done?

Well, maybe! But it is not that difficult either.

Why not prepare your next pitch along these lines and see the difference yourself?

Right ‘O then! Time to put on your black turtleneck?! 😊

This article on startup pitch in the Shark Tank India by the author first appeared in the 6th March 2022 edition of the English daily ‘The Hitavada’, in the business insights section of the Newscape supplement.

* in reference to the ONLY venture on the show that could justify its valuation and got funded at that valuation.

The image used is subject to copyright. Shark Tank India is a popular reality show by Sony Entertainment Network (SET). The article is not an advertisement of the show or its new Season 2 but an independent article by the author.

The car, coffee, and cosmetic examples illustrate that product differentiation is ephemeral. It has become transient. It is now more a hygiene factor than a source of sustainable competitive advantage.

So, if product differentiation is merely a hygiene factor, how to compete in the cut-throat marketplace?

To answer this question, let us go back to basics.

Consider our typical sales situation. Three entities are present here: the seller, the product (or service), and the buyer (or customer).

Here, many salespeople focus on the first two:

How they as seller are different

How their product is different

This is the seller-centric approach.

It focuses on sellers and their products.

It reminds me of a captivating scene in the movie The Wolf of Wall Street. When Jordan Belfort (Leo DiCaprio) asks some conference attendees to “sell me this pen”, they take this same approach.

“Sell me this pen” from the movie The Wolf of Wall Street

However, this seller-centric approach is suboptimal.

It may work in certain situations. But it isn’t ideal for building long-term customer relationships. Hence, it is not sustainable.

That brings us to the third entity present in the sales process – the customer.

Today, the customer has access to a lot more information at the touch of a screen. They can easily compare products and prices. If they don’t like something in a product, they switch just as easily. They know what is best for them.

In short, customers want to be in control of their buying process.

The problem is, the seller-centric sales does not do that.

Customer-centric sales is the approach that puts the customer’s needs and purchase motivations at the centre of the sales conversation.

In customer-centric sales, you don’t try to get people to buy your stuff they don’t need, by dwelling on seller or product differentiation.

Instead, you focus on knowing customers better. Make it data-driven. We call it developing customer intelligence. You strive to understand customers at a much deeper level.

Generally, salespeople know which customers buy their products?

But many times, they do not know ‘WHY do those customers buy their products.’ Unfortunately, this is more common than we think.

The key is to know the real reason and motive behind the purchase.

But, why is THE WHY important?

Because, customer’s reason to buy your product is likely to be different from your reason to sell it.

And guess what?

Your reasons to sell do not matter; while customers’ reasons to buy do.

This may sound harsh. But it is true.

You may be selling dog food because it is so good in quality that you can also eat. Whereas, the customer may be buying it because it is cheap and convenient.

You may be selling expensive maple wood furniture because the wood is durable and sourced from hardwood forests of North America. The customer may be buying it simply because it is lighter.

You may be selling homemade food as you have fresh organic homegrown ingredients. But the customer may be buying your homemade food because they can get it customised.

The point is this.

Customers buy anything for THEIR own reasons, not yours.

Businesses that get this insight embrace customer-centric sales approach and thrive.

Others that fixate on their own seller-centric differentiation without concern to customers’ reasons struggle.

Consider examples of a few companies where a seller-centric sales approach failed them.

Example 1: A video rental company closed because of not knowing their customer’s why.

You guessed it right.

Blockbuster was in the business of ‘renting out DVDs’. Their competitor Netflix also started ‘renting out DVDs’ in 1997.

Blockbuster’s model was seller-centric. It focused heavily on high street retail sales. Apart from other things, they maximised revenues by charging late returns (of DVDs). Blockbuster made 16% of their revenues in late fees.

On the contrary, Netflix pursued customer-centric sales strategy and studied customers. They enabled consumers to watch videos for a flat monthly fee without worrying about returns.

Blockbuster’s seller-centric model frustrated customers. Netflix’s customer-centric approach eased customers about returns.

Blockbuster vs Netflix

Meanwhile, faster internet allowed online streaming. It enabled customers to watch videos online. Ergo, customer buying preferences changed. They stopped going to stores altogether.

Eventually, Blockbuster ended up bankrupt. And Netflix emerged as one of the top ‘over-the-top content platforms.’

Source credit: Strategyjourney.com

According to the UK CMO of blockbuster Bryn Owen, Blockbuster’s sales-driven model did them in.

Example 2: “Share memories, Share life.” A Kodak moment (in 2012) that saddened everyone.

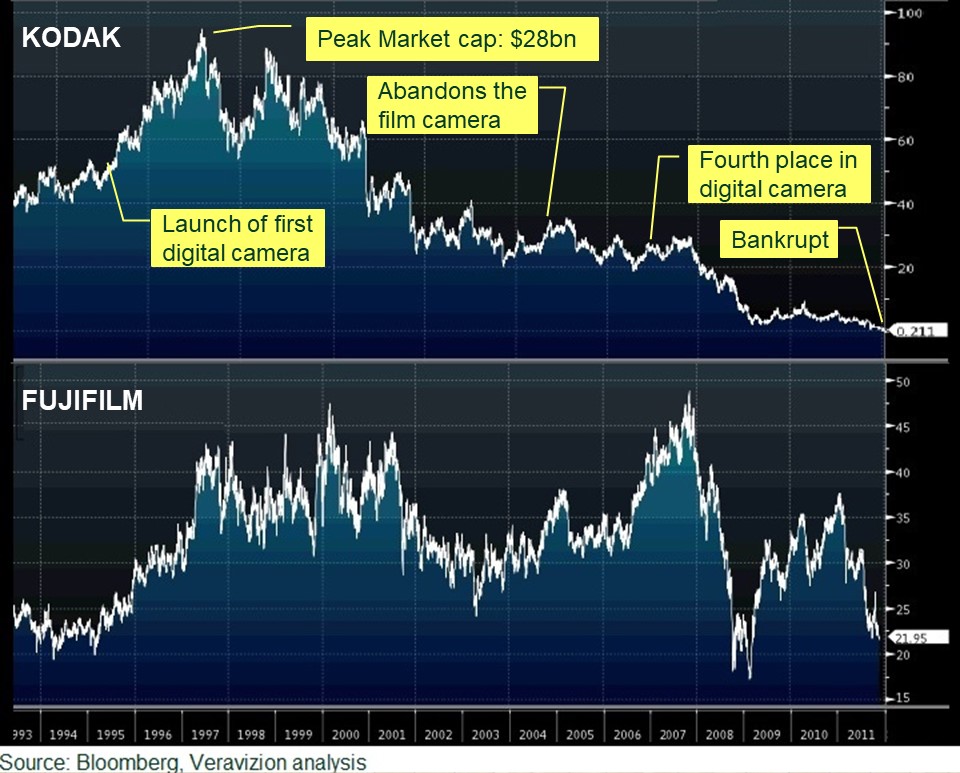

George Eastman, Kodak’s founder, invented roll film in 1888.

Kodak was primarily in the photographic film business. They prided on their silver-halide film technology.

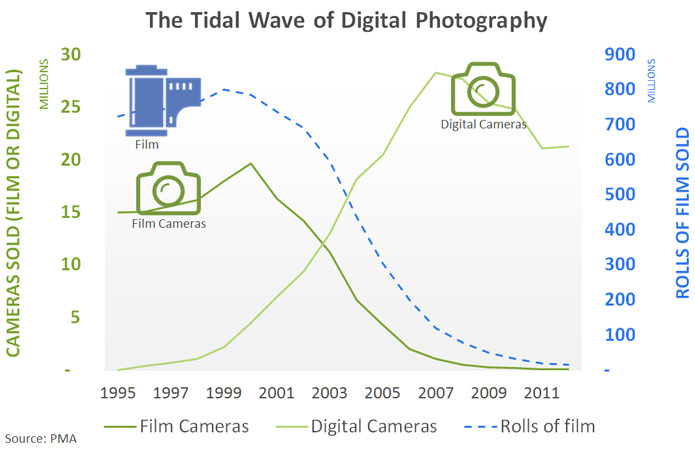

Listening to customer demand, Fujifilm started selling film in 1934.

Meanwhile, the digital revolution started in the 1960s.

Steve Sasson, the Kodak engineer, developed the first digital camera in 1975. Source credit: James Rajotte for The New York Times

By the late 1990s, the demand for photographic films dropped in line with the growing popularity of digital cameras.

Source: PMA, Business 2 community

The rapid spread of digital technology disrupted the photographic equipment industry.

Fujifilm invested in knowing customer’s changing preferences. They adapted to this shift by switching to digital lines of business.

Despite that, Kodak focused on film.

Not just that.

Kodak had acquired a photo-sharing site called Ofoto in 2001. If they were customer-centric, they would have been the pioneer of something like present-day Instagram.

Instead, Kodak used Ofoto to try to get more people to print digital images.

In the end, Kodak filed for chapter 11 bankruptcy in January-2012.

Kodak and Fujifilm stock performance comparison with key events.

Don Strickland, a former vice-president of Kodak, said: “We developed the world’s first consumer digital camera but we could not get approval to launch or sell it because of fear of the effects on the film market.”

Once the world’s biggest film company, Kodak became a posterchild for failure due to not being customer-centric.

Unfortunately, these aren’t isolated examples of companies stuck with seller-centric sales approach. GM, Nokia, Xerox, JCPenney, Palm, Sony are but to name a few.

Building a new competitive advantage with customer-centric sales

Building a true competitive advantage requires implementing customer-centric sales strategy. This strategy has these three benefits:

You give customers, control in their buying process

Customers get what they want

It is sustainable

Most internet-age companies that are growing rapidly are customer-centric.

Amazon obsesses over customers as they want to be known as Earth’s most customer-centric company. Everyone knows about customer-centricity of Google, Nordstrom, and Southwest.

Companies like Lululemon, John Lewis, and Target have invested in developing customer intelligence to be customer-centric.

So, how are these successful businesses pursuing this deliberate strategy of customer-centric sales?

Product differentiation is a strategy employed by businesses to achieve a competitive advantage by differentiating their products from those of their competitors.

Product Differentiation – why?

Generally, salespeople highlight their differentiation advantage to customers in two ways:

Our company is unique and special. Buy from our company.

This is seller differentiation.

Our product is unique and special. Buy our product.

This is product differentiation.

We will analyse seller differentiation later.

In product differentiation, special typically means high quality. The source of uniqueness and high quality in a product could be varied. Some of them are rare raw materials, advanced technology, distinctive design, superior personnel, or unusual methods. These become the sources of product differentiation. Customers perceive such products as high performance or exclusive. So, they are willing to pay a higher price for them.

Up until now, product differentiation helped businesses sell, and charge premium to their customers.

However, this is changing.

In a recent conversation with the CEO of a cosmetics company in Europe, he gave a thought-provoking perspective in the context of their product differentiation.

The CEO: “[First] it was ‘natural’. Then we introduced ‘natural fruit-based’. Then it became ‘natural fruit-based paraben-free allergen-free’. And it went on like that… Whenever I try to differentiate my product further, I feel I am narrowing my customer base. It is a big problem because my loyal customer base keeps shifting…”

Evidently, his concern is not misplaced.

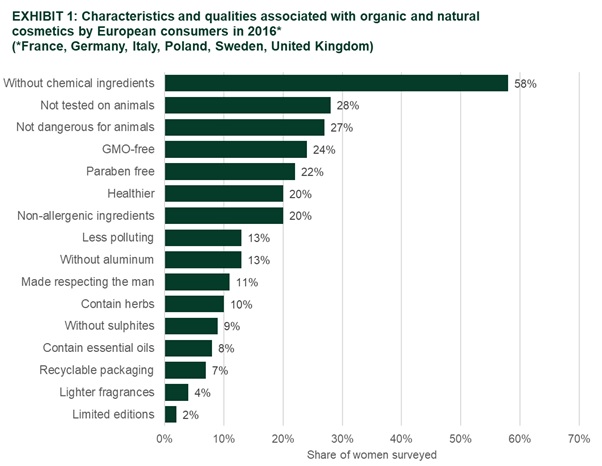

In an online survey in Europe, 900 women aged 25-65 years buying cosmetics and being interested in organic and natural cosmetics associated different characteristics and qualities with organic and natural cosmetics (see EXHIBIT 1).

Source: Statista 2021, Veravizion analysis

To be honest, this finding isn’t surprising.

There are so many ways to differentiate a product within a category. They may not appear truly differentiated at all.

It appears, product differentiation as a source of competitive advantage is losing its sheen. It may not be enough going forward to compete.

Wonder why it is so?

To find out, we analysed the sources of product differentiation. Our analysis yielded these insights.

In our increasingly global and digital world, the sources of product differentiation have become pervasive.

Global supply chains make it easy to procure raw materials from any place on the Earth. That too fairly quickly.

A free market economy facilitates the effortless movement of goods and expert personnel.

The Internet makes it simple to share information and technology.

Basically, it has become easy to procure stuff and change. This helps your rivals achieve parity with your products in no time.

Let’s see how.

Consider examples from three diverse product categories: cosmetics, coffee, and car. Notice how a product that once appeared differentiated from their competitors’ doesn’t seem so anymore.

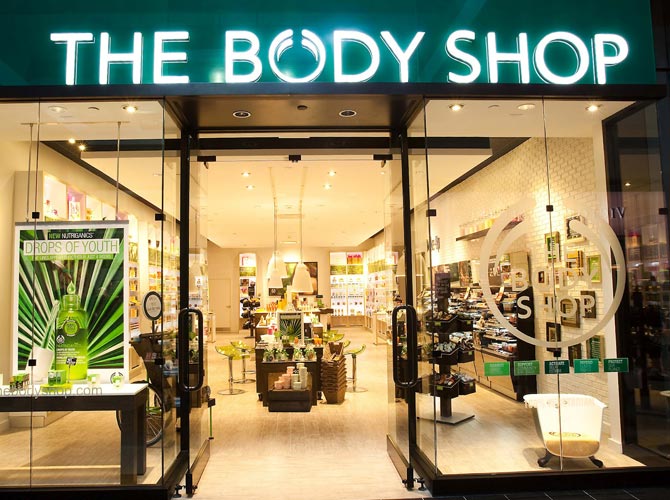

Example 1: The Body Shop – the first natural and organic cosmetic brand?

The Body Shop is perhaps the first global company to popularise the use of ‘natural ingredients’ in cosmetics. Anita Roddick, an activist, founded it to also promote ethical consumerism. The business’s original vision was to sell products with ethically-sourced, cruelty-free, and natural ingredients. The company was one of the first to prohibit the use of ingredients tested on animals. The Body Shop truly differentiated itself at the time. And it thrived. This was in the eighties and early nineties.

Source: The Body Shop

However, competitors followed suit soon after. Every cosmetic company wanted to show natural ingredients in their product. So much so that, it might be difficult to find a cosmetic company that does not seek to differentiate itself as natural or organic. Looks like, Natural is a hygiene factor in cosmetics now.

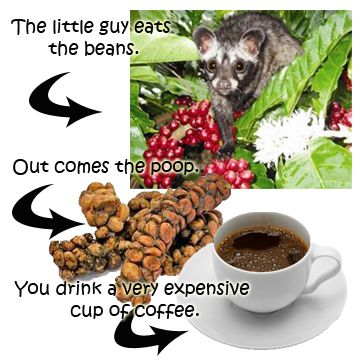

Example 2: Kopi Luwak – world’s most expensive coffee

Source: Pinterest

Civet coffee, also called Luwark coffee (or Kopi Luwak), is advertised as the world’s most expensive coffee. It is expensive because of an uncommon method of producing it. Civet coffee is produced from the coffee beans digested by civet cat. The faeces of this cat are collected, processed, and sold. A unique process indeed!

Civet coffee is originally from Indonesia. But, it is now produced across many countries in South East Asia. It is available in India too. It may only be a matter of time before we see this coffee in our favourite coffee shops. Moreover, there are other coffee brands such as Black Ivory, Finca El Injerto, Hacienda La Esmeralda, Saint Helena, and Jamaican Blue Mountain that are touted as the world’s most expensive coffee. Apparently, Kopi Luwak seems to have lost its flavour as world’s most expensive coffee.

Example 3: Exotic and handmade Phantom – an epitome of luxury

Source: Caranddriver.com

Rolls-Royce Phantom Coupé gained fame as your own bespoke exotic car handmade by expert craftsmen. Rolls-Royce claims that no two Phantoms in the world are exactly the same.

Finally, a true differentiator? We thought so too.

Only, there are at least ten other cars which take pride in calling themselves most exotic and handmade. Lamborghini, Bugatti, Pagani trump the track where Aston Martin is not even in the top-3.

Therefore, that forces us to ask.

Product Differentiation: is it a competitive advantage or a hygiene factor?

The point from the above examples is this.

The Body Shop might be natural and organic; Kopi Luwak might be a billionaire’s brew; Rolls-Royce Phantom might be exotic and handmade.

But they are not the only ones doing it in their industry. Rather, they join the crowd by competing on product differentiation.

Ironic, isn’t it!

The truth is this. The more you pursue product differentiation, the more you risk looking like the scores of your competitors doing the same.

It makes one wonder whether ‘our product is high quality’ has become a hygiene factor. It will not guarantee you sales, let alone premium prices. But not having it will definitely hurt sales.

But wait!

Apple pursues a product differentiation strategy. And Apple continues selling huge numbers of iPhones and iOS devices. In fact, iOS had more than 50% of the market share in the US as of May-2020 (see EXHIBIT 2).

Source: Statista

How do we explain this?

Clearly, something is at play here.

Is product differentiation a source of competitive advantage? Or has it merely become a hygiene factor?

If the latter, then how can you compete in the fiercely competitive marketplace?

In a sales situation, a salesperson looks to convince a customer to buy their (product or service) offering. To do that, they must showcase how their offering creates value for the customer. They are aware that the customer would be comparing their offering with those of their competitors. This is where the competitive advantage comes into the picture.

Competitive advantage renders you an edge over your rivals. A company’s competitive advantage makes their (product or service) offering more desirable to customers than those of their competitors.

According to Investopedia, competitive advantage refers to factors that allow a company to produce goods or services better or more cheaply than its rivals.

The factors could be price, product quality, delivery speed, customer service, location, and so on.

Among these, the price factor is different from the other factors.

Let’s see how.

Competitive Advantage: the ‘Price factor’

When a business competes on price, they price their products lower than their competitors’ prices. Therefore, they must produce the product at a low cost to sell it at a profit.

Source: Walmart.com

For example, Walmart competes on price. Their slogan is “everyday low prices”. They must produce or procure products at a very low cost to sell at a profit.

Competitive Advantage: the ‘Other factors’

When a business competes on factors other than price, they must ensure highdifferentiation from the competitors on that factor. Their slogan would be the best quality, higher speed, better customer service, and so on. However, it takes additional resources, and thus higher costs, to create differentiation. Hence, they must price the product at a premium to sell it at a profit.

Source: Christies.com

For example, dubbed as the world’s most coveted handbags, Hermès Birkin bags are super-expensive. Each bag is handmade by a single artisan craftsman using premium materials like calf skin, alligator skin, and even ostrich skin. And there is a waiting list for the top ones like the one shown here.

This low cost and high differentiation form the basis of business strategy for firms.

Porter defined these two ways in which an organization can achieve a competitive advantage over its rivals as costadvantageand differentiationadvantage.

Cost advantage & differentiation advantage served us well.

Thus far.

However, competitive advantage must be sustainable. It should help us sell in today’s fiercely competitive markets and tomorrows. In the absence of sustainable competitive advantage, your product may not continue to sell for long.

This is where the challenge is.

Both these sources of competitive advantage are seller-centric. They talk about seller’s cost advantage and seller’s differentiation advantage.

The thing is, competitive advantage for a business is the factor (or reason) for which the business wants customers to buy their products.

And the truth is, customers buy anything for THEIR own reasons, not yours.

Please do let the above two insights sink-in before you read ahead.

Therefore, it follows that, the factor for which a business wants customers to buy their products should be customer-centric.

That is, the source of competitive advantage for a business should be customer-centric (and not seller-centric).

This is like the movement of scientific theory from the Ptolemaic system (the earth at the centre of the universe) to the Copernican system (the sun at the centre of the universe).

It is a paradigm shift.

When that happens, a business will always be aligned with customer-needs. As and when the customer buying preference changes, a business will be able to respond to the change by correspondingly aligning their source of competitive advantage.

Savvy?! But wait.

What is the significance of this finding?

This signifies that the existing ways of building competitive advantage – cost and differentiation advantage – alone may not suffice.

The evidence is in the huge number of businesses shutting down, like Arcadia group, Chuck E. Cheese, Debenhams, J. Crew, JC Penny, Mamas & Papas, Mothercare, Neiman Marcus, and Wallis to name a few. Some of them are (sorry, were) iconic retailers. The list is long. Many of them are permanently closing most of their stores. Don’t we know that all of them had built competitive advantage the traditional way?

In short, we need to build the next frontier for developing sustainable competitive advantage.

Except, the ways of understanding a customer have undergone a sea-change. There is a lot more we can learn about a customer to help them.

Let us summarise the whole thing.

In the internet age, when brick-and-mortar businesses are finding it difficult to compete and are closing down, companies cannot rely only on the traditional meaning and sources of competitive advantage.

There is a need to build new frontier.

Developing your customer intelligence is the first step in that direction. That entails understanding many more things than we have ever known until now. This new frontier of competitive advantage helps you build a solid platform to grow further and beyond.

Besides, who has ever gone wrong knowing more about their customers?

Online business growth – the easy way or the right way?

Onine business growth is a topic concerning most retailers. How can retailers grow their business in these times? The key message is at the very end.

Consider this scenario.

You are the owner of a mid-sized retail business. You presently sell your product to your customers in physical stores. A typical sale goes like this: Customers show up at your store. They specify their needs, you give options. You counsel, they choose. You pack, they pay, and you complete the transaction.

Thus far, you have been successful in your current brick-and-mortar model. Your business has a loyal customer base. The net profit margin is in the range of 15%-20%. And, the cash flow is good too.

So, you decide to take your business to the next level.

How would you do it?

The answer is ‘yougo omnichannel’.

The internet penetration of above 90% in most developed countries makes it a no-brainer. Among the developing countries, the internet has grown by over 5000% since year 2000 to around 59%. Moreover, customers now prefer to buy in an omnichannel environment.

In omnichannel retail, the focus is on providing seamless shopping experience to the customer across multiple channels. Omnichannel strategy helps you integrate physical store, online store, mobile app, and social media.

In-short, your business growth strategy now revolves around selling online.

To sell online, there are two main options:

Create your ‘own online channel’

Sell through existing ‘online marketplaces’

This decision determines the future course of your business.

Let us dissect each option.

Option-1: Create your own online channel

Creating your own online channel includes two things: first, setting up an e-store – an e-commerce website – to display products and receive customer orders. Second, you need to have an efficient and trustworthy logistics system to fulfil the customer orders. The entire order-to-fulfilment process must run smoothly to give customers a seamless shopping experience.

Having your own online channel has several benefits.

Top three benefits are:

You can create bespoke personalised experience for your customers. It allows you to ensure stronger connection and engagement with them.

You have total control over your business throughout the customer buying process. So, you decide how customers interact with your brand while being on your website. Also, you can create relevant content around your offerings to engage with target customers.

Most importantly, you gain direct access to your customers and their data. You can leverage advanced analytical techniques to analyse this data. This analysis can give you crucial insights about the type of visitors, their visiting trends, and their buying patterns. These insights help you decode the online customer behaviour. Using that, you can make appropriate changes to the way you sell online. This data-driven online selling strategy promises to help you grow your online sales.

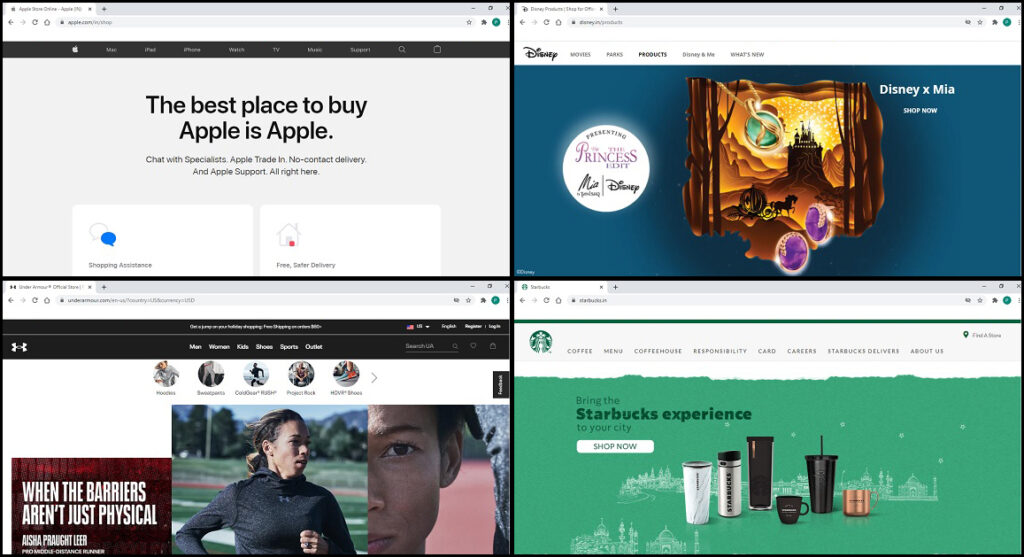

What do top-brands do?

While it is not a surprise that top brands like Apple, Starbucks, Disney, and Under Armour have their own online channels, most mid-size businesses have also launched their own online stores. It helps them create unique customer experience. The successful ones have implemented advanced analytics to reveal insights about their customer buying behaviour.

How top brands ensure unique and enjoyable customer experience through their e-stores

However, a common perception among small retailers is that there are a few disadvantages with this option, viz. higher upfront investment, additional analysis and marketing costs, and higher lead-time for online business growth. Perhaps, that is why, almost one-third of small businesses in the US do not have a website of their own.

That brings us to the second option.

Option-2: Sell through existing ‘online marketplaces’

Online marketplaces allow you to sell products without you having to set up your own online store. The marketplaces host many sellers on their website. Marketplaces are popular among buyers because they allow to buy different products across categories without having to leave the site.

The marketplace owns everything on their website. They take care of the marketing too. In return, you pay them product listing fees and a commission on every product sold.

There are many online marketplaces around. A few are global, some are regional, and many of them are national. The popular ones are Amazon, eBay, Flipkart, AliExpress, Rakuten, Etsy, and Target, amongst many others.

Many retailers tend to choose this second option over the first. It seems easier to them. Ostensibly, they see the following ‘advantages’ in this option – no upfront set-up cost, reduced marketing costs, and no waiting for online business growth.

Except, these advantages hide the real disadvantages.

Let us explain by listing out six key disadvantages of ‘selling through marketplaces’ option:

No Upfront cost = Lose control over sales

You don’t incur upfront cost if you don’t invest in your own e-commerce set-up. Instead, you use the marketplace’s infrastructure to sell. You use their e-commerce applications, their algorithms, and their processes. You depend on them for the sales.

Sure, the sales can increase, but you may not know why. [GE executives recall how Mr. Jack Welch would get angry when the sales went high and they couldn’t explain why.]

In a way, you lose control over your sales process and data to the marketplace.

Why is it a big problem?

Because, if the sales go down, you would be clueless about it. And so, would not know how to fix the problem.

Let us see an example of what it means by not having control.

When you are selling on marketplaces, you cannot control what products are being sold beside yours. Worse, what if the other product looks identical to yours but is from your competitor. Worse still, what if the other product being sold has the same brand-name as yours, but in altogether different category.

It DOES happen!

Here is a real example* of a brand selling at one of the top marketplaces:

The organic soft-cotton baby onesie, is selling alongside

woman’s cocktail dress of the ‘same’ brand-name (but from a competitor); selling alongside

motor flush oil of the ‘same’ brand-name; selling alongside

a music label of the ‘sam-e’ brand-name

– all of them in the same window.

And you cannot do anything about it.

Reduced analysis and marketing costs = Risking business survival

Generally, marketplaces own the data on your product sales. The minute a retailer signs up to a seller’s account on a marketplace, they give permission to the marketplace to use their sales data however they choose. Most marketplaces don’t share that data back with the sellers.

So, in reality, when you choose to sell through a marketplace, you don’t just pay listing fees and a commission per transaction. You also pay with your sales data, and future sales.

[I would re-read that last sentence to let it sink in.]

Marketplaces can use your sales data to gather your customer intelligence. They can leverage it to offer your customers better deals through their in-house labels.

Sellers have shared stories about how this has impacted their business.

In short, you risk losing your loyal customers to your competitors if you do not leverage your sales data yourself.

No waiting for sales-success = Less opportunity to build your brand

Online marketplaces try to make the seller onboarding process easy to bring more offline sellers on their e-commerce platform. They try to make it smooth and quick. You can start selling in a few days [and you may stop selling in fewer days if you violate their policies].

Not just that, you may also start realising sales quickly on marketplaces. However, the presence of many other products makes it difficult for consumer to register your brand among so many others in their minds.

You are successful quickly = Threat of getting undercut on prices

If you start doing really well, someone will notice and one of the two things may happen – they may offer to buy you out or they may undercut you on price and terms, eventually killing you.

Remember Zappos? Zappos was extremely customer-centric, very successful. It was the first company that sold shoes online, at scale. They put a lot of importance on understanding shoes, their culture and customer centricity.

When Amazon wasn’t going anywhere with its own online shoe store, Endless.com, they made their first attempt to acquire Zappos in 2005. Zappos declined. What happened later is not up in public domain. However, Amazon eventually acquired Zappos in July-2009.

Hyper-competitiveness – Forced to sell on price, not differentiation

Conservative estimates put the number of active sellers on Amazon at 2.3 million as of 2019. Chances are, many of them are selling the same products as you do. This makes it difficult for you to compete, if you do not have aggressive [read: less] pricing, that helps the algorithm pick your product ahead of the competitors’.

Diapers.com may be the case in point. They built a $100 million business selling diapers online. They offered free delivery of diapers and other products to parents. But they couldn’t sustain the competitive pressures and ceased to exist in 2017.

Restrictive TnC on how you can communicate with customers = Limits brand building

There may be marketplace limitations on how your business can brand and communicate itself on the marketplace. Moreover, any slightest hint of violating the strict policies will earn you the dreaded ‘seller suspension’ message.

Does that mean marketplaces are bad?

NO! Not at all.

In fact, they have disrupted some aspects of retail for the better.

For example, online shoppers love Amazon. Amazon is allowing them to have wider selection, shop-anytime-anywhere convenience, and enjoyable shopping experience, all at a cheaper price. They have developed a world-class e-commerce platform over the years.

Marketplaces can be good for small retailers, that do not have resources to have their own e-store. Also, marketplaces may be useful for those businesses not aiming to create an enduring brand.

But they may not be for everyone.

You need to figure out whether marketplaces are right for you.

Then, what is the way forward to online business growth?

Companies are waking up to the risk of increasing their dependency on marketplaces. More and more mid- and large-sized companies are embracing “direct-to-consumer” sales model.

Almost all large businesses and brands have their own e-commerce stores. Some of them were tempted initially but then recovered themselves from increasing their dependency on the marketplaces.

Nike – just doing it without a marketplace!

Nike is one such example. Recently, Nike confirmed to CNBC that it will stop selling merchandise directly to Amazon, as part of its push to sell more directly to consumers.

To quote CNBC, “Prior to 2017, Nike had resisted such a deal with Amazon, focusing its attention on its own online marketplace and stores. The fear for many brands has always been that, by partnering with Amazon, a company loses control over how its brand is represented on the site.”

This Veracle makes a point that mid-sized businesses should strive to have their own e-commerce set-up. They should attempt to leverage their sales data using analytics. This could be the right way for their online business growth.

What do you think? Have you seen a mid-sized business struggle with this dilemma?

Customer shopping behaviour is an important concept in retail.

This is why.

How do you grow your retail business? You sell what customers want. How do you know what customers want? Well, you observe how they buy.

When customers buy a product or service, they do certain things. First, they search for the product online or in stores. Next, they try to seek more information and compare prices. Then, they check product ratings and seek feedback from friends. Over time, they engage with brands through social media.

All the actions mentioned above describe customer shopping behaviour.

Customer shopping behaviour in e-retail refers to how customers interact with your website. It involves understanding the actions a customer performs between landing on your website and leaving.

So, how exactly do we “observe customers”?

We do this using the various Key Performance Indicators (KPIs). KPIs help us get a sense of real-situation quantitatively.

Now, we can measure the customer shopping behaviour in e-retail using the following KPIs:

Total visits

Bounce rate

Shopping cart abandonment rate

Shopping cart conversion rate

Sales conversion rate

Average duration on page

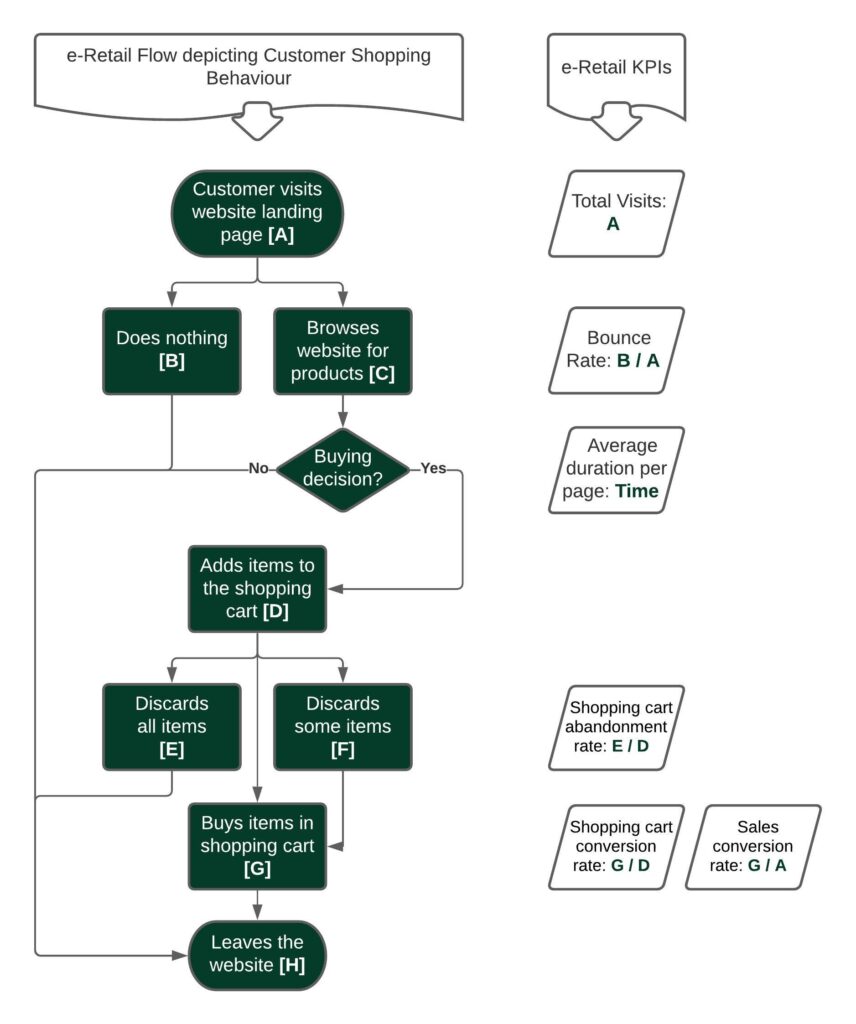

The flowchart in the figure below illustrates these actions. The little boxes on the right of each process show the corresponding KPI.

Flowchart depicting customer shopping behaviour in e-retail

Customer Shopping Behaviour KPIs in e-retail

Here is a brief explanation of each KPI.

Total Customer Visits

Total visits KPI is the total number of visitor landings on a website.

According to Google, 63% of all shopping begins online. That makes ‘Total Visits’ the vital first KPI for an e-retail sale. E-retailers try to increase this KPI to increase sales.

Bounce Rate

Bounce rate is the proportion of visitors landing on your website and leaving without taking any action.

If the website is engaging for customers, they interact with it. More the interaction, lower is the bounce rate, and better are the prospects of making a sale.

There are various reasons for a high bounce rate. Moreover, a high bounce rate doesn’t tell the entire story. Also, there are ways to improve it.

Shopping cart abandonment rate

This KPI means a customer added products in their e-retail shopping cart but later abandoned the order.

According to Statista, 63% carts were abandoned because shipping cost was too high. While these customers have not yet purchased, they are most easy to convert to a sale.

Shopping cart conversion rate

Similarly, this metric helps e-retailers measure the number of completed orders compared to the total number of shopping carts initiated by potential customers.

It is calculated as a ratio of number of visitors who placed an order, to the total number of visitors who started a shopping cart. It is expressed as a percentage.

Sales conversion rate

Google defines sales conversion rate as the ratio of transactions to sessions, expressed as a percentage.

The recent Adobe Digital Index 2020 report pegs average global conversion rate in retail at 3% of the total visits. The sales conversion rate varies across various retail categories. Conversion of consumer electronics is only half at 1.4%. Gifts, and Health & Pharmacy generate the highest conversion rates at around 4.9%.

Average duration per page

One e-retail KPI to measure is the time spent on each webpage. This is tracked as ‘average duration per page’.

This KPIs is based on similar one in traditional retail. In physical retail store, more the time a customer spends inside a shop, higher are the chances of purchase.

So, what do you think? Do you track these metrics? If yes, which ones do you think are the most important for your business?

How are E-Retail KPIs different from traditional Retail KPIs?

What is E-Retail KPI?

E-retail is the online website of a retail store. KPI means Key Performance Indicators. So, the key performance indicators for an online website of a retail store are e-retail KPIs.

Traditional retail is a physical brick-and-mortar retail store. Let’s call their KPIs, traditional retail KPIs.

E-retail and traditional retail by their nature are different. The difference exists from two perspectives: the customer perspective and the retailer perspective.

Let us see the customer’s perspective first.

The customer perspective drives their shopping preferences and buying behaviour. For instance, customers who value convenience, price comparison, time-saving, and the ability to shop 24×7 prefer to shop online. Whereas, customers who want to touch, feel, and try the product first tend to shop in physical stores.

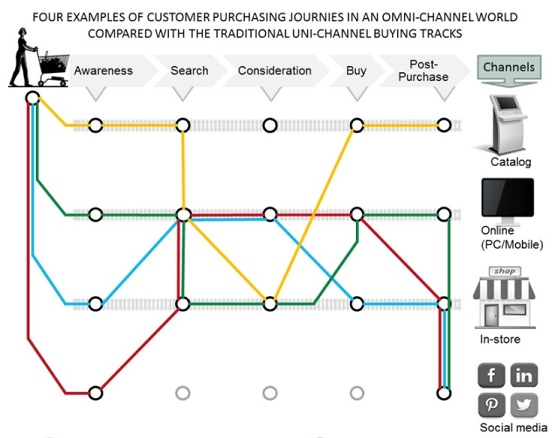

Increasingly, customers are buying in an Omnichannel environment. Omnichannel means all channels work seamlessly as one. That is, they discover a product in one channel, check it out in another one, and buy through a third. Such as shown in the figure below.

Omnichannel shopping is becoming the norm

Now, the retailer perspective.

The retailer’s perspective influences their business operating behaviour. Traditional retailers focus on maximizing the in-store experience for their customers while optimizing store space. While e-retailers focus on the online shopping experience and user personalization.

These two perspectives influence their KPIs.

How E-Retail KPIs Differ?

Many e-retail KPIs are common with traditional KPIs. Some of these are the various financial ratios, customer retention, and conversion rate. However, e-retail KPIs are different from traditional retail KPIs in two major areas:

Customer Acquisition Channels

Customer Shopping Behaviour

Let us see how.

Customer Acquisition Channels

This is the source of customer traffic to your business. Understanding where your customers are coming from is extremely important for business growth.

E-retail channels are primarily organic search, direct search, referral, e-mails, and social media. These channels actually lead customers to e-retail stores (i.e. the website). So, e-retailers can easily measure the percent of customers acquired from these channels. They can then devise their deliberate strategy around these insights.

For example, Facebook generates 13.9% of e-retail website traffic, but actual sale happens in only 4.7% of cases. This is a critical piece of information in two ways: First, it allows you to allocate resources efficiently. Also, it improves ROI.

Traditional retail channels are different.

They are mainly word of mouth or advertisements in print, television, radio, and social media. For traditional retailers, it is nearly impossible to accurately calculate the percent of customers acquired from these different channels. This is because these channels do not ‘redirect’ them to the store.

For example, a customer actually visiting a store may have seen an ad or may have been referred by word of mouth. But, they may not even remember this information when they visit the store.

Customer Shopping Behaviour

Customer behaviour varies a lot between in-store purchases and online purchases. Understanding customer behaviour is central to acquiring more customers.